Open any mid-year allocator survey and you meet the same five trends: the end of 60/40, the retreat from US concentration, geopolitics as a portfolio variable, the private-markets liquidity squeeze, and liquid alternatives as the new ballast.

They are real. By now they are also consensus, and naming them tells a manager nothing a competitor's deck does not already say. The useful work begins one layer down, where each trend hides a gap between the portfolio an allocator describes and the one they actually hold. Those gaps are not closing evenly. They look different in London, Amsterdam, Sao Paulo and New York, and that variance is the most precise demand signal in the market right now.

The dataset: The figures below come from 515 institutions across 29 countries, drawn from Natixis, J.P. Morgan, BlackRock, the ECB and McKinsey, read against our own daily map of where allocations are moving and which managers are winning mandates.

01 · Portfolio Architecture

The 60/40 is gone. What is replacing it does not have a rulebook yet.

Stock-bond correlation turned deeply positive after the Middle East conflict, reaching 0.72 in late March, the highest since 2024, stripping bonds of their hedge precisely when it was needed. The response is structural, not tactical: 71% of institutions now expect a 60/20/20 mix to beat the traditional 60/40. They are adding hedge funds, infrastructure, private credit and return-seeking fixed income, while cutting large-cap US equity.

The gap: A 20% alternatives sleeve has been bolted onto portfolios faster than the governance to run it. Many books look diversified on paper but hold two correlated risk factors in practice. Almost no committee has rewritten its risk framework for the sleeve it just bought.

Regional pulse

- ▶UK: Furthest along. Post-LDI pension funds have cut duration and are rotating into private credit and infrastructure under the Mansion House agenda; scheme consolidation is building pools large enough to run complex alts.

- ▶EMEA: The architects. Dutch and Nordic giants (ABP, PFZW, AP funds) lead on alternatives-augmented design; Gulf SWFs are recycling oil revenue into longer-duration return streams.

- ▶Lat Am: Slowest. Chilean and Peruvian AFP reform restricts offshore allocation; Brazil (PREVI, PETROS) is the exception, pivoting hard into local private credit as real rates compress.

- ▶US: The endowment model is being copied by mid-market foundations and public pensions. CalPERS and CalSTRS lifted alts targets materially under funded-status pressure.

What allocators want from managers

- ✓Regime modelling: Show how the strategy behaves when bonds and equities sell off together, not just in normal markets.

- ✓Architecture: Offer modular sleeve solutions, not isolated single-strategy pitches.

- ✓Governance: Partner on the framework for the new 20% sleeve, not just the product that fills it.

02 · Geographic Allocation

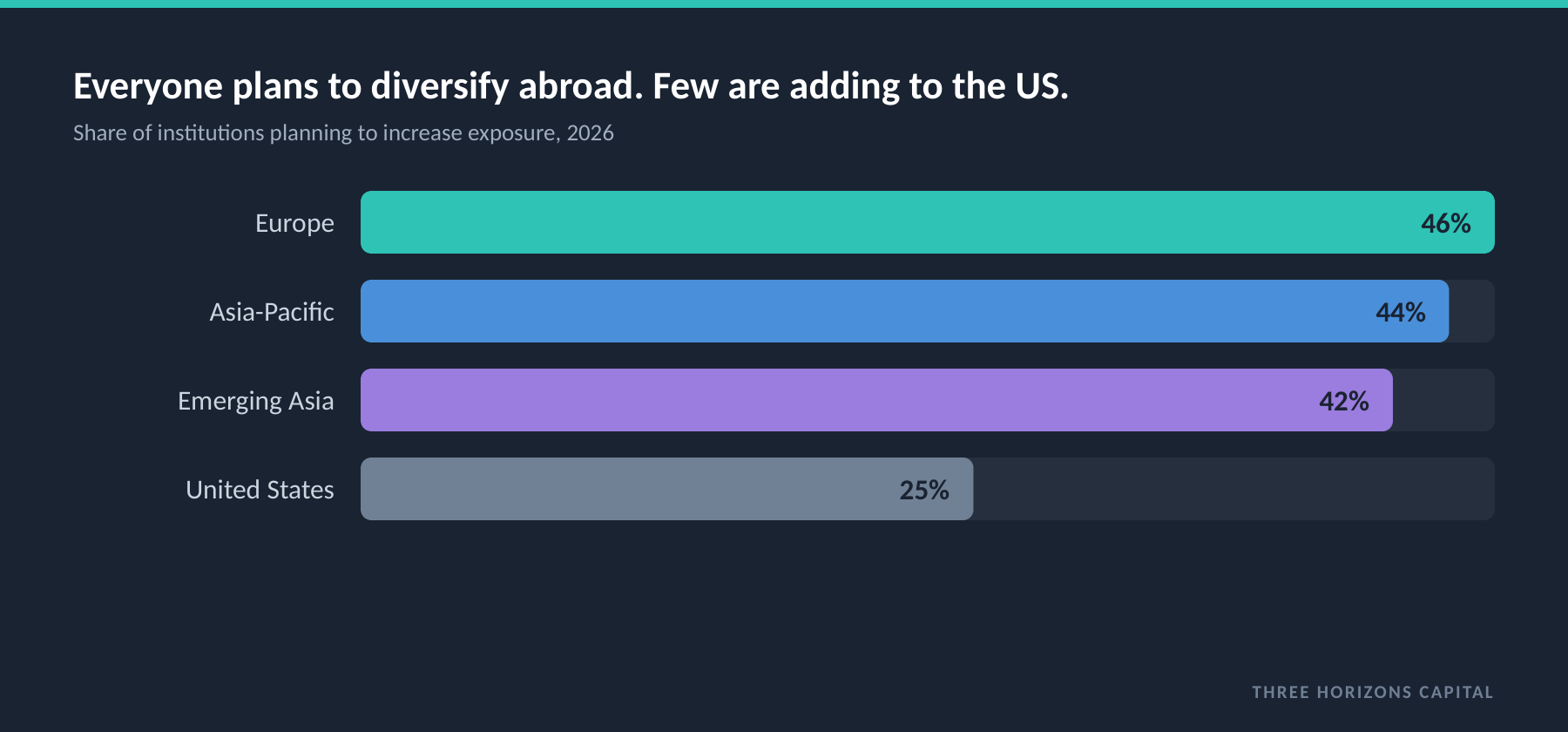

Everyone says cut US concentration. They are overweight, and still buying.

The ten largest stocks now make up 38.4% of the S&P 500 and dominate the MSCI World, leaving passive global investors heavily concentrated in a handful of US technology names. Nearly half of institutions plan to diversify away.

The gap: Intent and exposure have come apart. The same allocators who plan to diversify keep adding to US large-cap, because a strong dollar flatters the returns and nothing else offers the liquidity. The real dilemma is reducing concentration without surrendering AI-driven earnings, and most have not resolved it.

Regional pulse

- ▶UK: Caught between politics and merit. The Mansion House Compact pushes UK-listed equity, but the FTSE 100 is value and energy heavy and does not solve technology diversification; UK-to-Europe allocations are growing as a substitute.

- ▶EMEA: Already underweight US large-cap relative to global peers, and benefiting from it in 2026. MENA sovereigns are building pan-African and South Asian books as a deliberate multipolar strategy.

- ▶Lat Am: The most constrained. Chile, Colombia and Peru cap cross-border equity; within the limits the trend is intra-regional infrastructure, with Brazil adding Indian and South-East Asian equity.

- ▶US: Foundations and endowments are revisiting home bias after the early-2026 tariff shock; books that had drifted past 70% US are being rebalanced toward Japan and European quality.

What allocators want from managers

- ✓True active share: Deliver genuine regional mandates, not repackaged global strategies; prove active share against the MSCI World.

- ✓Currency nuance: Offer local-currency variants with transparent hedging cost.

- ✓Concentration math: Show, at portfolio level, exactly how much mega-cap technology risk a non-US allocation actually removes.

03 · Macro & Risk

Geopolitics is "a core variable." Pricing never got the memo.

The Iran conflict has proven protracted, driving oil above $100, pushing back central-bank easing and pressuring equities. While 45% of US institutions name geopolitical disruption as their top fear, global private equity multiples rose from 11.3x to 11.8x EBITDA through the same period.

The gap: The fear is in the survey, not in the price. Deal documentation still treats geopolitical risk as a checkbox, and few LPs have stress-tested illiquid books against a prolonged Strait of Hormuz closure or wider escalation. Lock-ups with no force-majeure provisions expose portfolios to a scenario nobody has modelled.

Regional pulse

- ▶UK: Treating defence and European rearmament as a theme, not only a risk; adding defence-linked infrastructure and energy security, with the Ukraine ceasefire trajectory dominating committee agendas.

- ▶EMEA: The most sophisticated. Dutch and Nordic funds are running formal China-Taiwan scenario overlays for the first time; Gulf SWFs treat the conflict as both risk and windfall and recycle accordingly.

- ▶Lat Am: Watching US-China decoupling most closely given trade exposure to both; Brazilian and Chilean funds are stress-testing copper and lithium volatility, and positioning nearshoring as the regional opportunity.

- ▶US: The most outspoken on China. Endowments are cutting Hong Kong-listed and direct China PE under board-level pressure; tariff uncertainty adds a domestic dimension to the modelling.

What allocators want from managers

- ✓Hard overlays: Bring named scenario overlays, not a generic risk-factors paragraph; model the illiquid book against a Hormuz closure or a China blockade.

- ✓Structural safety: Build force-majeure provisions directly into fund documentation.

- ✓Themed capture: Position defence, energy transition and nearshoring as investable themes, not abstract headlines.

04 · Private Markets

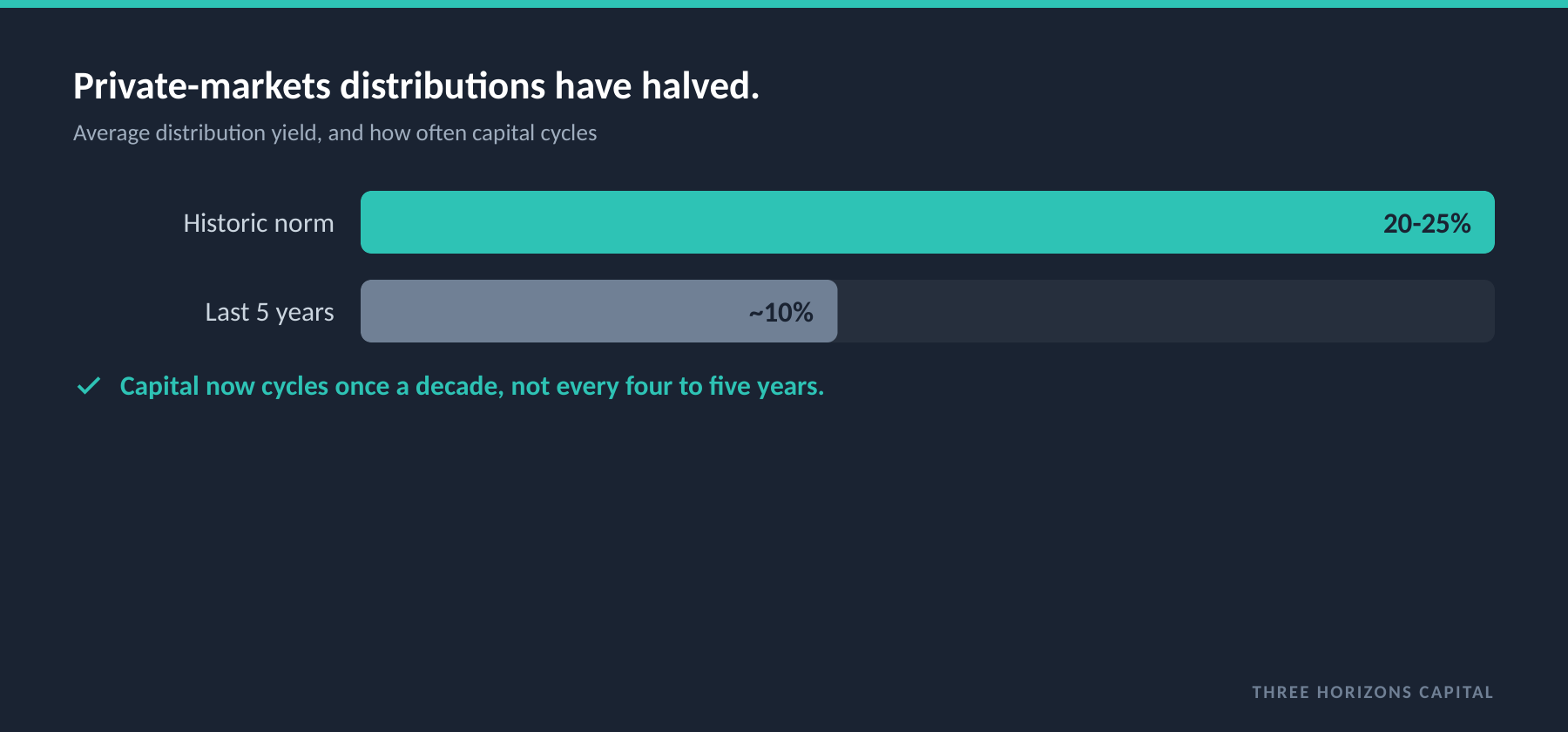

A record allocation arrived just as the cash stopped coming back.

Institutions are committing 12.5% of portfolios to private markets, the highest on record, and 88% plan to hold or increase it. The conviction is real, and so is the strain underneath it. Capital cycles half as often as it used to.

The gap: Rising allocations, lengthening lock-ups, constrained exits and redemption-gate stress are converging at once. Open and semi-open credit funds are testing their gates. The secondary market has become an active management tool rather than a last resort, and most committees have not run a full liquidity-mismatch scenario against the book they are still adding to.

Regional pulse

- ▶UK: Balancing the productive-finance push against post-LDI liquidity duty; British Business Bank and LGPS pools are emerging as major commitments, and retail access via LTAFs is just beginning.

- ▶EMEA: ELTIF 2.0 has opened private markets to a broader wealth segment; Dutch and Swiss funds run the most sophisticated programmes and manage liquidity actively via secondaries, with Gulf SWFs now buying.

- ▶Lat Am: Access is regulator-constrained outside Brazil, where pension funds are deploying into domestic infrastructure and credit; regional fund-of-funds structures are gaining as a denominator-safe route.

- ▶US: The most exposed to the distribution drought; actual cash-flows are running below pacing-study models. Allocators are concentrating with fewer, larger managers, and the BDC market is under NAV-mark scrutiny.

What allocators want from managers

- ✓Real liquidity: Offer evergreen structures with genuine provisions, not windows that gate at the first sign of pressure.

- ✓Standard secondaries: Provide a dedicated secondaries programme as a built-in LP service.

- ✓Valuation transparency: Deliver transparent NAVs with independent marks, alongside LP-side pacing models.

05 · Liquid Alternatives

The new ballast is already crowding.

Interest in liquid alternatives as a diversifier jumped by half after the Middle East conflict. Global macro and multi-strategy are now judged as portfolio shock absorbers rather than pure alpha vehicles. Replacing part of a bond allocation with hedge funds has moved from heresy to mainstream thesis on the back of higher inflation and the equity-bond correlation breakdown.

The gap: The diversification is being bought just as it gets scarce. When multiple systematic funds run similar signals, their correlation spikes at exactly the wrong moment. Allocators are searching for genuine structural uncorrelation and finding the supply narrower than the demand, which means much of what is bought as ballast is the same trade in a new wrapper.

Regional pulse

- ▶UK: The UCITS wrapper provides the governance and daily liquidity trustees require; managed futures and global macro lead, and wealth managers are adding liquid alts to model portfolios at the GBP250k-plus segment for the first time.

- ▶EMEA: Gulf family offices and SWFs are among the most active new allocators, favouring global macro and longer-vol; Dutch funds are sizing up rather than starting; Solvency II insurers favour AIFMD-compliant alts.

- ▶Lat Am: Access is largely via UCITS or US 40-Act funds; Brazil, Mexico and Colombia family offices are the primary buyers, valuing CTA and macro as a currency hedge against BRL, COP and MXN volatility.

- ▶US: Endowments are the most sophisticated users, running liquid alts as a tactical complement to manage overall liquidity ratios; RIAs are building them into wealth models on client demand for equity protection.

What allocators want from managers

- ✓Uncorrelation proof: Show structural uncorrelation, not low beta in a bull market; publish rolling correlation against equities and bonds across regimes.

- ✓Capacity discipline: Commit to explicit capacity caps and hard closes.

- ✓Track record: Show a multi-regime record that includes both the 2022 and 2026 drawdowns.

The thread

Five trends, one problem

Read together, these are not five stories. They are one. The portfolio an allocator describes in a committee meeting has moved faster than the portfolio they actually hold, and the distance between the two is where the risk sits and where the next decision waits.

The 20% alts sleeve without a risk framework, the diversification everyone plans and few execute, the geopolitical fear that never reached the price, the record private allocation with halved liquidity, the ballast that is quietly crowded: each is a stated strategy that has outrun its own implementation. The gap is closing at a different speed in every region. A manager who treats the world as one market will bring the wrong product to three of those five rooms. The manager who wins the mandate is not the one who can name the trend. It is the one who can show the allocator the gap, in their own region's terms, and bring the specific thing that closes it.

How Three Horizons Capital helps close the gap

Real-book stress testing

We run an allocator's current book against the five scenarios above, an oil shock, a China decoupling, a private-credit gate, an EM rally and stagflation, and show the impact on expected return and Sharpe across eight major capital-market-assumption providers at once.

True factor mapping

We show which of a book's alternatives are genuinely uncorrelated and which are the same Growth, Inflation or Liquidity bet repackaged, so a diversified sleeve can be seen for what it really is before the next drawdown reveals it.

Regional demand scoring

We score any fund on philosophy, process, people and performance, flag crowding risk and manager tenure, and cross-reference it against the regional allocator demand signals above, so a manager knows which strategy fits which room.

One honest point: these are point-in-time figures from third-party surveys and primary sources taken at mid-2026. Survey intentions and fund flows can reverse when the headline that drove them resolves. We would rather say so than imply the picture is fixed.

Sources: Natixis IM Global Institutional Survey 2026; J.P. Morgan Q2 2026 Global Allocation Views and long-term capital-market assumptions; BlackRock Spring Investment Directions; ECB Financial Stability Review, May 2026; McKinsey Global Private Markets Report (private equity multiples). Coverage: 515 institutions, $29.9 trillion, 29 countries. For platform demonstration and research purposes; not investment advice.